AMFI-Registered Mutual fund Distributors

AMFI-Registered Mutual fund Distributors

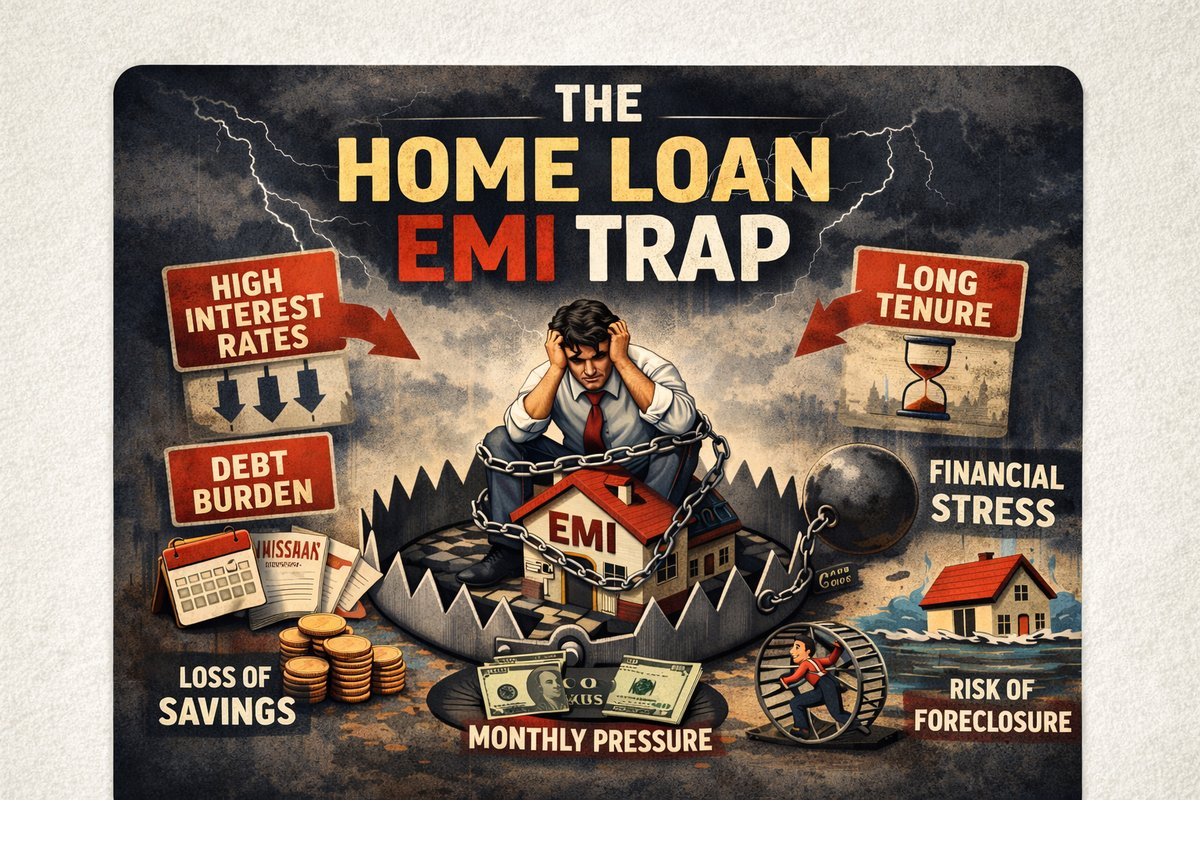

How a low monthly payment can cost you more than the house itself — and what smart borrowers do differently.

You got the keys. The EMI feels manageable. But buried in the fine print is a number nobody highlighted — the total amount you'll pay back. Often, it's nearly double what you borrowed.

Home loans are the largest financial commitment most Indians will ever make. Yet the way they're sold — with low monthly EMIs and tax benefit promises — conceals the real cost. This article dismantles every layer of the EMI trap, and gives you the tools to beat it.

An Equated Monthly Installment (EMI) is designed to feel affordable. Banks optimize for a number that fits your monthly budget — not for minimizing your total outgo. The trap is simple: the longer the tenure, the lower the EMI, but the higher the total interest paid. Most borrowers optimize for the wrong variable.

On a ₹50 lakh loan at 9%, choosing 30 years over 15 years saves you only ₹12,000/month in EMI — but costs you an extra ₹55+ lakhs in interest over the loan's life.

The most insidious trap is the belief that a longer tenure is "safer." Here's what the math actually says across different tenures for the same ₹50 lakh loan at 9% interest:

| Tenure | Monthly EMI | Total Amount Paid | Total Interest | Interest as % of Principal |

|---|---|---|---|---|

| 10 Years | ₹63,338 | ₹76,00,560 | ₹26,00,560 | 52% |

| 15 Years | ₹50,714 | ₹91,28,520 | ₹41,28,520 | 83% |

| 20 Years | ₹44,986 | ₹1,07,96,640 | ₹57,96,640 | 116% |

| 25 Years | ₹41,799 | ₹1,25,39,700 | ₹75,39,700 | 151% |

| 30 Years | ₹40,231 | ₹1,44,83,160 | ₹94,83,160 | 190% |

Notice: going from 10 to 30 years saves just ₹23,107/month in EMI — but costs an additional ₹68.8 lakhs in interest. You are essentially buying two houses instead of one.

The bank doesn't care how much you pay in total. They care about whether you can pay each month. Your goal is the opposite.

Home loans use a reducing balance method, which sounds fair — but the amortization schedule means you pay mostly interest in the early years. For a ₹50L / 20-year / 9% loan:

| Year | Annual EMI Paid | Goes to Interest | Goes to Principal | Balance Remaining |

|---|---|---|---|---|

| Year 1 | ₹5,39,832 | ₹4,43,921 | ₹95,911 | ₹49,04,089 |

| Year 3 | ₹5,39,832 | ₹4,25,344 | ₹1,14,488 | ₹46,29,044 |

| Year 5 | ₹5,39,832 | ₹4,03,987 | ₹1,35,845 | ₹43,10,282 |

| Year 10 | ₹5,39,832 | ₹3,39,561 | ₹2,00,271 | ₹34,48,162 |

| Year 15 | ₹5,39,832 | ₹2,45,789 | ₹2,94,043 | ₹22,03,447 |

| Year 18 | ₹5,39,832 | ₹1,53,241 | ₹3,86,591 | ₹12,86,504 |

| Year 20 | ₹5,39,832 | ₹48,190 | ₹4,91,642 | ₹0 |

In the first 5 years, over 74% of every rupee you pay goes toward interest. You barely dent the principal. This is why selling or refinancing early rarely helps — your outstanding loan amount barely moves.

Most home loans today are on floating rates linked to the RBI repo rate. When rates rise, banks have two choices: increase your EMI, or extend your tenure. Guess which one they usually do.

| Scenario | Original Rate | New Rate | Bank's Action | Your Cost |

|---|---|---|---|---|

| Rate hike (1%) | 8.5% | 9.5% | Tenure extended ~3 yrs | +₹12–18L interest |

| Rate hike (2%) | 8.5% | 10.5% | Tenure extended ~7 yrs | +₹28–35L interest |

| Rate cut (1%) | 9% | 8% | Usually passed on slowly | -₹10–15L if proactive |

What to do: After any rate hike, call your bank and explicitly ask them to maintain the same tenure — even if it means a slightly higher EMI. Never let tenure silently extend without your notice.

Many borrowers take a larger loan or longer tenure because "the tax benefits make it worth it." Let's do the actual math:

| Parameter | Reality Check |

|---|---|

| Max deduction under Sec 24(b) | ₹2,00,000/year on interest |

| Tax saved (30% bracket) | ₹60,000/year maximum |

| Interest paid in Year 1 (₹50L loan) | ~₹4,44,000 |

| Actual tax saving | ₹60,000 (not ₹1,33,000) |

| Net out-of-pocket interest cost | ₹3,84,000 |

| Worth paying extra interest for? | Never |

For every ₹100 extra you pay in interest, the government reimburses at most ₹30 (if you're in the 30% tax bracket). You are still losing ₹70. Tax benefits are a consolation prize, not a strategy.

| Hidden Cost | Typical Amount | When It Hits |

|---|---|---|

| Processing fee | 0.25%–1% of loan | At disbursement |

| Legal/technical charges | ₹5,000–₹15,000 | At disbursement |

| Prepayment penalty (fixed rate) | 1%–2% of prepaid amount | When you prepay |

| Balance transfer charges | 0.5%–1% | When switching lender |

| Home loan insurance (bundled) | ₹50,000–₹2,00,000 | At disbursement |

| MOD (Memorandum of Deposit) | ₹1,500–₹5,000 | At disbursement |

| MODT charges (some states) | 0.1%–0.2% of loan | At disbursement |

The single most powerful tool against the EMI trap is prepayment. Even one extra EMI per year has a dramatic effect:

| Prepayment Strategy | Effective Tenure | Interest Saved | Loan Closes |

|---|---|---|---|

| No prepayment (base case) | 20 years | — | 2045 |

| 1 extra EMI/year | ~17 yrs | ~₹9.5L | 2042 |

| ₹10,000 extra/month | ~14 yrs | ~₹22L | 2039 |

| ₹25,000 extra/month | ~10 yrs | ~₹36L | 2035 |

| Annual bonus (₹1L/yr) | ~16 yrs | ~₹14L | 2041 |

Based on ₹50L loan @ 9%, 20-year tenure, starting 2025.

| Year | Opening Balance | Principal Paid | Interest Paid | Closing Balance | % of EMI → Interest |

|---|

Target an EMI that is 35–40% of your net monthly income — not 25%. The short-term pain saves lakhs.

Every bonus, increment, or windfall should go toward the principal first. Even ₹10,000 extra/month cuts 6+ years off a 20-year loan.

After every rate hike, ask your bank for an updated amortization schedule. Insist on maintaining original tenure by increasing EMI.

If a competitor offers 0.5%+ lower rate, consider transferring — but calculate break-even point first (processing fee vs. interest saved).

Top-up loans feel cheap because they're at home loan rates. But they reset your debt and can add years to your repayment journey.

Ask for it on Day 1. Know exactly how much is going to interest each month. Awareness alone changes spending behavior.

Your total home loan repayment (EMI × months) should ideally not exceed 1.6× the principal. Above 1.8×, you are firmly in the trap. Above 2×, reconsider the tenure or the loan size entirely.

Welcome to COGNITY WEALTH, a one-stop destination for comprehensive and dependable financial solutions. In a world where financial decisions shape life’s most important milestones, we aim to make those decisions easier, smarter, and more rewarding.

221 , Second Floor , Sebiz Infotech Private Limited , Sector 67 , Mohali Pincode - 160062

|