Your Bank is Paying You 3–4%.

Inflation is Taking 6%.

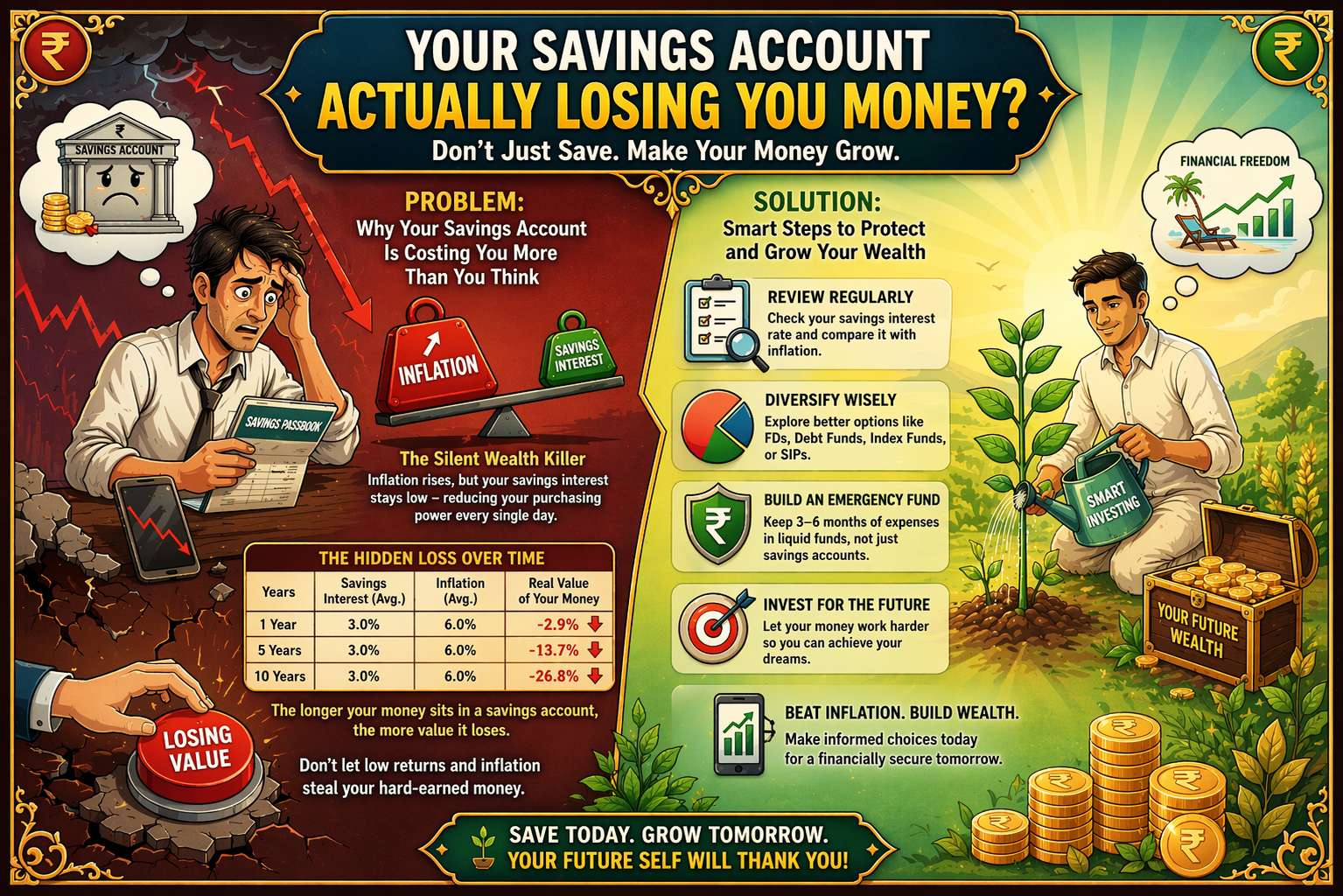

Let's be straightforward. Most major Indian banks — including SBI, HDFC, ICICI, and Axis — currently offer a savings account interest rate of 2.70% to 4% per annum. Some small finance banks offer more, but the large banks that most families use? It's firmly in that 3–4% range.

Meanwhile, India's Consumer Price Index (CPI) inflation has been hovering around 5–6% per annum over the past few years. Food inflation — the thing that actually hits your kitchen — has been running even higher at times.

So what happens when your money earns less than inflation is taking?

Imagine you could buy a bag of groceries for ₹1,000 today. Inflation means that the same exact bag of groceries will cost you ₹1,060 next year. Your money didn't disappear. The prices just went up — and your ₹1,000 can now buy less than it used to. That's inflation.

| Metric | What You're Getting | Verdict |

|---|---|---|

| Savings Account Interest (avg.) | 3.0% – 4.0% per year | Below Inflation |

| CPI Inflation Rate (approx.) | ~5.0% – 6.0% per year | — |

| Food Inflation (periodic highs) | 7% – 9% (seasonal) | — |

| Small Finance Bank Savings Rate | 6.5% – 7.5% | Closer to Inflation |

What Actually Happens to Your Money Over 5 Years?

This is where it gets real. Let's take ₹1,00,000 — a round, honest number — and see what two different futures look like.

Think of it like this: you have ₹1 Lakh today and you put it in the bank. Five years later, the bank hands you back ₹1.16 Lakh and says "Well done!" But the shops have also gotten more expensive. That same set of things you could have bought for ₹1 Lakh now costs ₹1.34 Lakh. Your ₹1.16 Lakh is not enough. You've lost ground — even though the number in your passbook went up.

In simple terms: your money grew, but your purchasing power shrank. The bank didn't cheat you. Inflation did its quiet work while your savings slept.

The Real Rate of Return —

Your True Financial Scorecard

Real Rate of Return

Economists use a simple concept to measure whether your money is truly growing or secretly shrinking. It's called the Real Rate of Return.

For a savings account earning 3.5% when inflation is 6%:

That negative number means you are losing 2.5% of your real purchasing power every year. Not gaining.

The Grocery Basket — A Story in Two Acts

Here is the most honest way to understand this. Forget interest rates and percentages for a moment. Think about groceries.

500g Ghee • Vegetables

Rice • Cooking Oil

Same shop.

Same quantities.

But you need ₹338 more.

Your savings account will give you ₹1,159 for that same ₹1,000. But the groceries cost ₹1,338. You are ₹179 short. That is the real rate of return — felt in your kitchen, not just in a spreadsheet.

Your money earns 3.5% interest. But everything around you gets 6% more expensive every year. So your money is actually shrinking at 2.5% a year — even though the bank says it's growing. That 2.5% gap? That's what economists call a negative real return. Your passbook lies to you with a smile.

Two Simple Alternatives for Your Idle Cash

Before we talk about equity, SIPs, or long-term investing — let's solve the most basic problem: idle money sitting in a low-interest savings account. Here are two practical solutions that are safe, liquid, and better than doing nothing.

Liquid Mutual Funds

These are mutual funds that invest your money in very short-term, high-quality debt instruments — think government securities and AAA-rated papers maturing in 91 days or less.

✓ Can be redeemed in one working day (some funds offer instant redemption up to ₹50,000)

✓ No exit load after 7 days

✓ Better post-tax returns than savings accounts (indexation benefit for longer holds)

✓ Ideal for emergency funds and short-term parking

Sweep-in Fixed Deposit

Many banks offer a feature where your savings account is linked to an FD. Any money above a certain limit (say ₹25,000) is automatically "swept" into an FD and earns FD interest.

✓ Works automatically — no action needed after setup

✓ FD is broken in reverse (last-in, first-out) when you need cash

✓ DICGC insured up to ₹5 Lakh

✓ Best for those who prefer full capital protection

A Liquid Fund is like keeping your money in a smart piggy bank that earns better interest while you sleep — and you can take the money out the next morning if you need it. A Sweep-in FD is like asking your bank to automatically move your extra money into a better savings jar, and it moves it back instantly when you need to pay for something. Both are safe. Both earn more than a regular savings account. Both let you sleep peacefully at night.

Important: These options are not replacements for long-term investments in equity mutual funds or SIPs. They are solutions specifically for idle cash — your emergency fund, money you'll need in the next 3–12 months, or just funds sitting untouched in your savings account. Every rupee has a job to do. Make sure yours are working.