1. What’s unique about investing in India?

India offers a high-growth potential economy but comes with specific nuances such as currency risk (for NRIs/Foreigners), a well-defined regulatory framework governed by SEBI, unique tax structures like capital gains with indexation benefits, and markets influenced by domestic politics, monsoons, and global FII flows.

2. What are the prerequisites before I start investing in India?

- PAN Card: Mandatory for all financial transactions.

- Bank Account: A linked savings account (preferably with net banking).

- KYC Compliance: Mandatory verification via online e-KYC or in-person.

- Demat & Trading Account: Required to buy/sell stocks and ETFs.

3. What is a Demat Account?

A Dematerialized (Demat) Account holds your shares and securities in electronic format, similar to how a bank account holds money. It is maintained with a Depository Participant (DP) such as Zerodha, ICICI Securities, HDFC Securities, or Angel One.

4. What is a Trading Account?

A Trading Account allows you to place buy and sell orders on stock exchanges. It is provided by your broker and linked to your Demat and bank accounts for seamless settlement.

5. What are the key investment avenues in India?

- Equity (Stocks): Shares listed on BSE or NSE.

- Mutual Funds: Professionally managed pooled investments.

- Fixed Deposits: Low-risk bank or post office deposits.

- PPF: Long-term, tax-free, government-backed scheme.

- NPS: Retirement-oriented and tax-efficient investment.

- Real Estate & Gold: Physical or via ETFs and REITs.

6. What is a Systematic Investment Plan (SIP)?

A Systematic Investment Plan (SIP) is the cornerstone of mutual fund investing in India. It allows you to invest a fixed amount at regular intervals (monthly or quarterly) into a mutual fund. SIPs promote financial discipline, reduce market timing risk, and benefit from rupee-cost averaging. You can start investing with as little as ₹500 per month.

7. What are ELSS funds?

Equity Linked Savings Schemes (ELSS) are equity-oriented mutual funds that offer tax benefits under Section 80C of the Income Tax Act, allowing deductions up to ₹1.5 lakh per year. These funds have a mandatory lock-in period of 3 years, which is the shortest among all 80C tax-saving options, while offering long-term wealth creation potential.

8. Who regulates the Indian markets?

The Securities and Exchange Board of India (SEBI) is the primary regulator of Indian financial markets. SEBI is responsible for protecting investor interests, promoting fair and transparent market practices, and regulating stock exchanges, brokers, mutual funds, and other market participants.

9. Is my money safe in the stock market?

- Shares & Debentures: Your securities are held securely in your Demat account, which is independent of your broker.

- Mutual Funds: Your units are held with the Mutual Fund Trust or in your Demat account, not with the distributor. Asset Management Companies (AMCs) operate under strict SEBI regulations.

- Broker Risk: SEBI-registered brokers must maintain client funds in segregated accounts, reducing misuse risk.

10. What are the big risks in Indian markets?

- Market Volatility: Sharp movements may occur around elections, budgets, or global economic events.

- Liquidity Risk: Small-cap and penny stocks may have limited buyers.

- Currency Risk (for NRIs): Exchange rate fluctuations between INR and foreign currencies.

- Regulatory Changes: Taxation rules and investment regulations may change with government policies.

11. What are the main costs of investing?

- Brokerage: Fee charged per trade. Discount brokers often charge very low fees (e.g., ₹20 per trade or around 0.03%).

- Demat Account AMC: Annual Maintenance Charges typically range between ₹300 to ₹1,000 per year.

- Mutual Fund Expense Ratio: Annual fee charged by the Asset Management Company (AMC) as a percentage of assets. Always compare this before investing.

- STT (Securities Transaction Tax): Mandatory tax levied on equity transactions. This cost cannot be avoided.

- GST: Applicable on brokerage, Demat AMC, and mutual fund management fees.

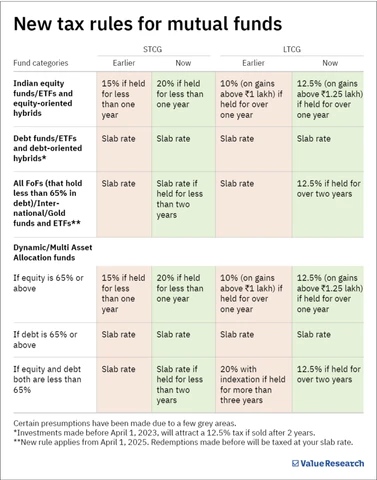

12. How are investments taxed in India? (FY 2025–26)

13. What is Indexation?

Indexation is a key benefit for long-term debt investments. It allows you to adjust the purchase cost of an investment for inflation using government-notified Cost Inflation Index (CII) values. By increasing the purchase price for inflation, your taxable gains reduce, thereby lowering your tax liability.

14. How do I start as a complete beginner?

- Complete your KYC through a broker or mutual fund platform.

- Open a Demat and Trading account with a low-cost broker.

- Begin with a SIP in a diversified equity mutual fund or an index fund.

- Gradually learn, review, and diversify across asset classes.

15. What are some classic mistakes to avoid?

- Investing without a goal: Always define objectives like retirement, home purchase, or education.

- Chasing tips and hot stocks: Avoid SMS or WhatsApp tips. Rely on research and fundamentals.

- Ignoring asset allocation: Don’t put all money in one asset type. Maintain a balanced mix.

- Timing the market: Regular SIPs are more effective than trying to buy at the lowest point.

- Not reviewing investments: Review your portfolio performance at least once a year.

16. What is the role of a financial distribution service in India?

A financial distribution services helps investors plan, invest, and manage their money efficiently based on goals and risk appetite. In India, you may work with a SEBI-registered Investment Guidance (RIA) or a Mutual Fund Distributor.

- RIAs: Charge a transparent fee for support and are legally required to act in the client’s best interest (fiduciary).

- Distributors: Earn commissions from the products they sell.

Always ask for guidance about their registration status and compensation structure.

17. How should NRIs invest in India?

NRIs can invest in India by following specific regulatory requirements:

- NRE/NRO Account: Mandatory for routing investments.

- NRI Demat & Trading Account: Required for equity investments.

- PIS Permission: Needed for repatriable stock investments.

- Taxation: NRIs are subject to Indian capital gains tax with higher TDS. Double Taxation Avoidance Agreements (DTAAs) may provide relief.

18. What are "smallcase" and "thematic investing"?

- Smallcase: Curated baskets of stocks or ETFs based on a theme or strategy (e.g., Digital India, Low Volatility). Investors can buy or track the entire basket in one click.

- Thematic Funds: Mutual funds that focus on specific sectors or trends such as infrastructure or banking. These are higher-risk compared to diversified funds due to concentration.

19. Is Gold a good investment in India?

Gold holds cultural and financial importance in India, but modern investment forms are more efficient:

- Physical Gold (Jewellery): High making charges, storage concerns, and lower liquidity.

- Gold ETFs & Gold Mutual Funds: Cost-efficient, liquid, and secure. Held in Demat format.

- Sovereign Gold Bonds (SGBs): Issued by the Government of India. Offer 2.5% annual interest plus gold price appreciation. Capital gains are tax-free if held till maturity (8 years).