AMFI-Registered Mutual fund Distributors

AMFI-Registered Mutual fund Distributors

Investing builds wealth. Structured withdrawal planning protects it.

A Systematic Withdrawal Plan (SWP) is one of the most efficient ways to generate regular income from mutual funds — provided it is aligned with current taxation rules and long-term asset allocation.

An SWP allows you to withdraw a fixed amount at regular intervals (monthly, quarterly, annually) from your mutual fund investment.

Important: You are redeeming units — not earning “interest”. Tax applies only on the capital gains portion, not the entire withdrawal amount.

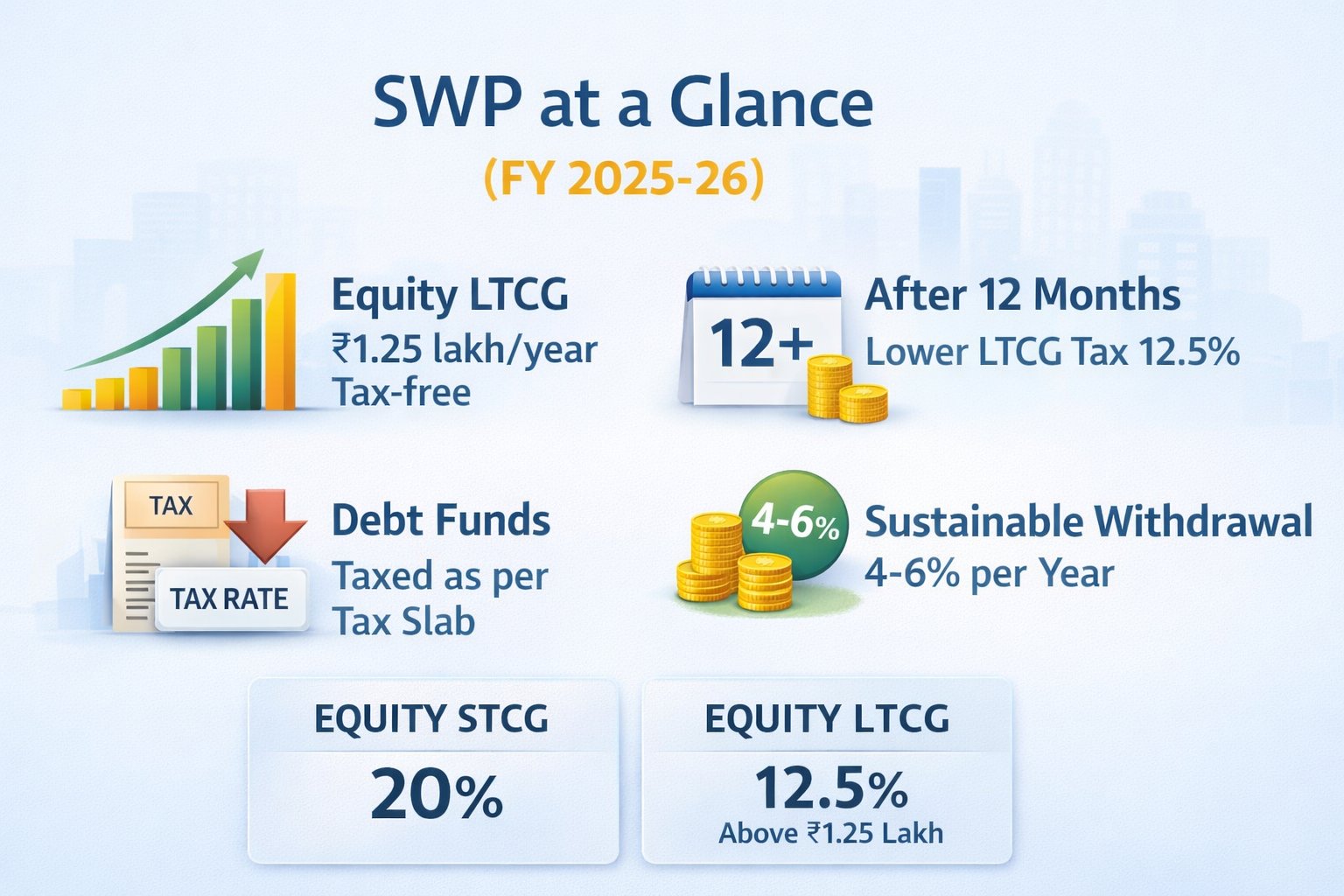

Tax treatment depends on whether the mutual fund is equity-oriented or debt-oriented.

| Particular | Tax Treatment (FY 2025-26) |

|---|---|

| Holding ≤ 12 months | STCG @ 20% |

| Holding > 12 months | LTCG @ 12.5% |

| Annual LTCG Exemption | First ₹1.25 lakh per financial year tax-free |

| Tax Applicability | Only on capital gains portion |

Key Insight: If your annual LTCG stays within ₹1.25 lakh, no tax is payable.

| Particular | Tax Treatment |

|---|---|

| Any holding period | Taxed as per income tax slab |

| Indexation benefit | Not available |

| LTCG benefit | Not applicable |

For investors in higher tax brackets, debt funds may be less tax-efficient for SWP compared to equity-oriented funds.

Practical Strategy: Invest → Complete 12 months → Then initiate SWP.

Initial Investment: ₹20,00,000

Current Value: ₹26,00,000

Monthly SWP: ₹25,000

Annual Withdrawal: ₹3,00,000

Capital Gain Portion: ₹1,10,000

| Particular | Amount |

|---|---|

| Total LTCG | ₹1,10,000 |

| LTCG Exemption | ₹1,25,000 |

| Taxable LTCG | ₹0 |

| Tax Payable | ₹0 |

Result: Entire withdrawal becomes effectively tax-free.

| Corpus | 5% Annual Withdrawal | Approx Monthly Income |

|---|---|---|

| ₹30 lakh | ₹1,50,000 | ₹12,500 |

| ₹50 lakh | ₹2,50,000 | ₹20,800 |

| ₹1 crore | ₹5,00,000 | ₹41,600 |

In long-term planning, a 4–6% withdrawal rate is generally considered sustainable.

| Feature | SWP | IDCW |

|---|---|---|

| Taxation | Capital gains only | Taxed as per slab |

| Control Over Amount | Investor controlled | AMC declared |

| Tax Efficiency | Higher | Lower |

| Compounding Impact | Better | Reduced |

Under FY 2025-26 tax rules:

When implemented correctly, SWP becomes a tax-aware income strategy — not just a withdrawal method.

— Team CognityWealth

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Tax laws are subject to change. Investors should consult their tax advisor for personalised advice.

Welcome to COGNITY WEALTH, a one-stop destination for comprehensive and dependable financial solutions. In a world where financial decisions shape life’s most important milestones, we aim to make those decisions easier, smarter, and more rewarding.

221 , Second Floor , Sebiz Infotech Private Limited , Sector 67 , Mohali Pincode - 160062

|